The ability to exclude gain on qualified small business stock (QSBS) under Section 1202 is becoming a more popular topic. However, the companion tax benefit under Section 1045 is much less well known. Section 1045 allows taxpayers to defer gain from QSBS held for at least six months by rolling the gain into another QSBS — essentially a like-kind exchange of QSBS. While Section 1202 is limited to $10 million or 10x basis, the Section 1045 gain deferral doesn’t have a cap. When combined with Section 1202, you may be able to get gain deferral on the sale of qualified stock today and the potential for a complete exclusion of the deferred gain in the future. There is a very quick timeline required to execute on investing in replacement stock under Section 1045. To make the most of this tax-planning opportunity, it’s important to begin planning for the reinvestment of proceeds as early as possible.

What are the requirements for Section 1045, and how is it different from Section 1202?

There are several requirements to take advantage of Section 1045. First, the deferral only applies to QSBS, which is generally defined similar to Section 1202. (The specific requirements of QSBS under Section 1202 are discussed in our previous article.) The one key difference from Section 1202 is that the stock only has to be held for six months rather than five years. Once the six-month holding period on QSBS is met, then a shareholder recognizing gain on the QSBS must reinvest the proceeds from that sale in other QSBS (replacement stock) within 60 days and make a proper election on their timely filed tax return for the year of the reinvestment.

How does Section 1045 work?

Shareholders reinvesting proceeds from QSBS into qualified replacement stock can reduce or eliminate the gain on the sale of the QSBS. At its core, Section 1045 is a gain deferral provision — a shareholder is choosing to pay taxes in the future rather than in the year of the original sale. To accomplish this deferral, the basis of the replacement stock is reduced by the deferred gain, increasing the gain that will be recognized on sale of the new stock in the future. Since the replacement stock may be held for years into the future, the gain deferral may be very long term.

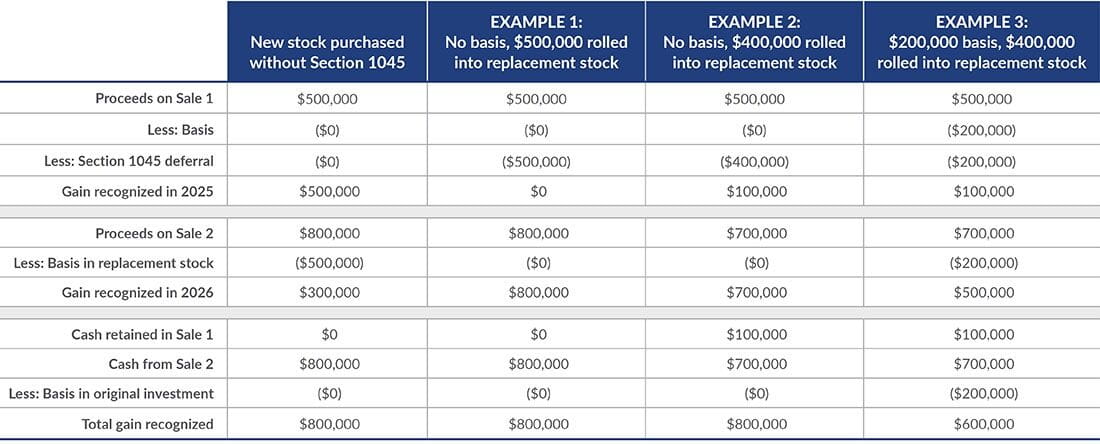

Magnifying the power of Section 1045 by combining it with Section 1202

While Section 1045 is primarily a gain deferral provision, careful planning into Section 1202 could allow that deferral to translate to a permanent exclusion. In a perfect world, the replacement stock would continue to meet Section 1202 requirements through the future sale of the stock. The replacement stock retains the holding period of the original stock, so it only needs to be held for the remainder of the five years required for Section 1202 in order to eventually qualify for the 100% gain exclusion.

Partnerships and Section 1045

A partnership that sells QSBS may also be able to make a Section 1045 deferral election if it reinvests in other QSBS within 60 days of its sale, but there are additional requirements in that scenario. Alternatively, a partner in that partnership could also reinvest into other QSBS directly, but they still need to do it within 60 days of the partnership’s sale of its original QSBS. In addition, it’s possible for a partner in a partnership that sells QSBS to make an investment in new QSBS through a separate partnership owned by that partner. Ultimately, there’s a lot of flexibility under these rules with respect to partners and partnerships, but the devil is in the details. The strict 60-day deadline requires a lot of communication between the partnership and its partners, as well as coordination on the timing of cash distributions to ensure that actions are taken in a timely manner.

Planning for reinvestment

The 60-day reinvestment requirement is often the biggest impediment for taxpayers to maximize the benefit of Section 1045. Unless ripe investment opportunities already exist when the initial sale occurs, it’s often difficult to identify and close a new investment in 60 days. Planning ahead can make a meaningful difference. For example, if the taxpayer is struggling to find replacement QSBS, the taxpayer can create a new corporation and invest the QSBS proceeds into that new entity. However, new stock only qualifies as replacement stock if the QSBS requirements are met for substantially all of the first six months following investment. Taxpayers that are considering forming a corporation should be prepared to begin active business operations quickly and deploy the invested capital or risk losing qualified small business status. Simply forming a corporation with a cash investment and holding onto that cash isn’t a good strategy. The key is that any actions taken regarding Section 1045 typically need to be arranged long before the 60-day reinvestment window even begins.

What to do now

Despite some of the limitations, Section 1045 can benefit taxpayers who initially planned to qualify for Section 1202 but end up not meeting the five-year holding period. Taxpayers may also be able to utilize Section 1045 in combination with Section 1202 to achieve robust tax-planning solutions when there are multiple investment tranches or where the total gain exceeds Section 1202 limitations. If you’re interested in the nuanced calculations of Section 1045, continue reading on.