Whether you’re starting a new business, looking for new investment opportunities, considering a sale of your business, or rethinking your existing structure, Section 1202 could be right for you. While this tax strategy is designed to be a benefit to small business owners, a business doesn’t have to be very small to qualify. And unlike many other tax rules, gain that’s excluded from taxable income (also known as the qualified small business stock exclusion or QSBS) isn’t deferred until later; and the tax savings are permanent. But before trying to take advantage of this tax benefit, take note — qualifying can be complex, so it’s critical to get a solid understanding first.

Section 1202: What does this mean for you?

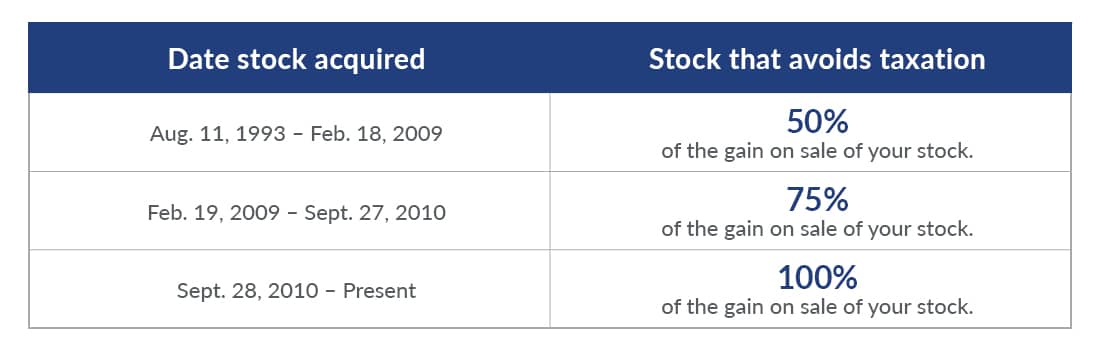

If you acquired your Section 1202 stock after September 2010, you can permanently exclude up to $10 million of the gain on sale of your stock. Based on a 23.8% federal capital gains tax rate and 4.2% assumed state income tax rate, you could potentially save $2.8 million or more in federal and state taxes. If the stock was acquired after July 4, 2025, you can permanently exclude the increased amount of $15 million and potentially save $4.2 million. The $15 million exclusion is subject to inflation adjustments beginning after 2026.

Additionally, if you’ve invested more than $1.5 million, that exclusion increases to 10 times your basis. For example, if you invested $5 million, your gain exclusion can be $50 million.

For stock acquired between 1993 and 2010, the amount of gain that avoids taxation can be 50 or 75%, depending on when the stock was acquired.

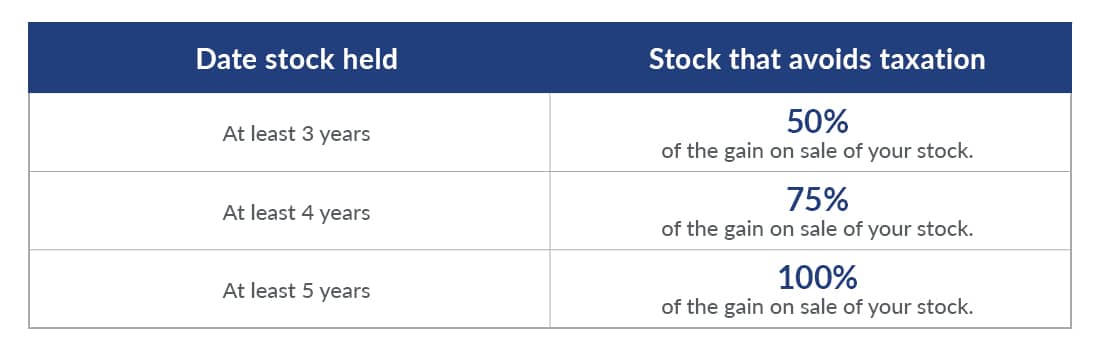

For stock acquired after July 4, 2025, the gain exclusion percentage depends on the ultimate holding period.

While each state differs, many states follow the federal gain exclusion or have their own rules, which can compound your potential savings.

Section 1202 criteria: How do you qualify?

The Section 1202 exclusion can apply to stock owned by individuals, trusts, or estates, and it can be owned directly or through a flow-through entity. Almost any owner can benefit except for C corporations. In order to qualify:

- The stock must be acquired via a direct investment in a C corporation.

- The stock must be held for at least three years from the date of investment.

- The corporation’s assets must be less than $75 million at the time of investment for stock received after July 4, 2025, or $50 million for stock received prior to that date (and at all times prior to the investment). The $75 million asset limit is subject to inflation adjustments beginning after 2026.

- The business must use at least 80% of its assets in a qualified trade or business, which includes all businesses except for:

- Professional service businesses

- Banking and financing

- Farming

- Oil, gas, and mining

- Hospitality

- Real estate & other passive businesses

Other requirements must also be met, so be sure to refer to the guidance or get help from a tax expert.

Ready to maximize your Section 1202 tax savings?

While Section 1202 tax savings come with some complexity in determining and protecting qualification, we can help you navigate these rules.

We’ll evaluate your situation, ensure that you have the proper documentation, and maximize your tax savings on the time, energy, and capital you’ve invested in your business. Contact us today to identify whether your business is maximizing potential tax savings under Section 1202.