First, the bottom line: Decent jobs report won’t move the needle on investor focus.

- There were no significant alarm bells in the March jobs report, but the numbers continue to point to a gradual easing in labor conditions.

- Unemployment is creeping up, but slowly. Job creation perked up in March, but downward revisions to previous data provides greater context around labor trends, which are easing. Layoffs haven’t risen considerably, but the pace of hiring has become choppier while also slowing.

- More concerning than the March jobs report, which was “good enough,” is the near-term outlook for the labor economy given the broader macro backdrop. That’s in a state of flux, with far more questions than answers about the ultimate impact of tariffs on inflation and how businesses and consumers will react.

- Add it all up — what would have otherwise been a decent jobs report will carry little weight for investors against the larger questions and growing uncertainty around the near-term outlook. Given the downside risk and range of potential outcomes, employers are likely to become more guarded in their hiring practices in the near term.

- Investors aren’t focused on what happened last month; it’s the recent speed, magnitude, and potential fallout of policy changes that’s been driving the markets. That focus isn’t likely to change any time soon, and the March jobs report isn’t going to move the needle in that regard.

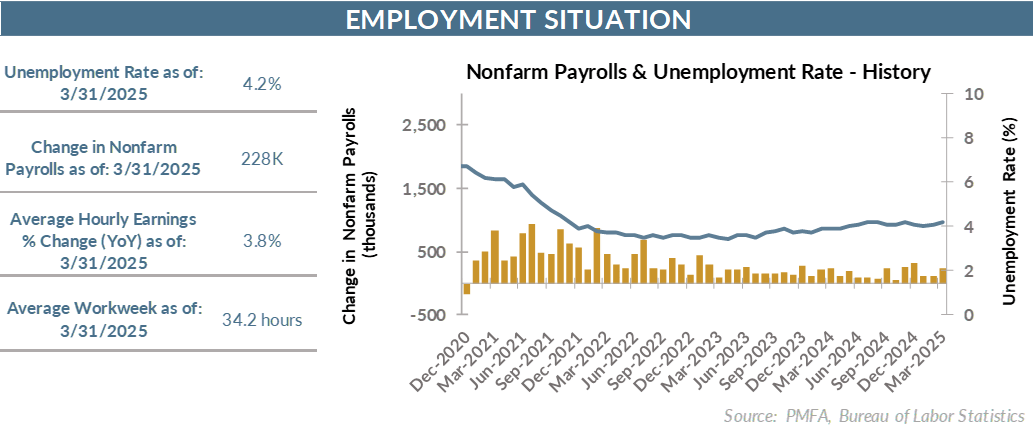

By the numbers: Solid March numbers dimmed somewhat by downside revisions.

- Job creation was much better than anticipated in March, coming in at a solid 228,000, easily topping forecasts for 140,000. However, the narrative changes a bit once the revisions to January and February totals are factored in, as those trimmed 48,000 jobs from the previously reported monthly gains. In total, the net 180,000 increase still topped forecasts, but to a much more limited degree.

- Job creation was particularly strong in the service sector, which added 197,000 jobs for the month. Manufacturing employment grew incrementally but has changed little since the end of last year.

- Perhaps most surprisingly, government employment rose by 19,000, although that was overwhelmingly driven by increases and the state and local level. Federal payrolls declined by 4,000, while still coming in 14,000 higher than the level a year ago.

- Unemployment stair stepped up from 4.1% to 4.2% in March, matching the high-water mark reached three times in the latter half of 2024. Even so, that’s a reading that’s consistent with a labor market at or near full employment.

- Wage growth continues to slowly ease, rising by 0.3% in March. Average hourly earnings over the past year grew by 3.8% — a solid advance, but not one that’s less likely to be a cause for concern from an inflationary perspective.

Broad thoughts: It’s the uncertainty.

- Over three decades ago, James Carville made famous the quote, “It’s the economy, stupid” as the answer to what was top of mind for voters. Today, the answer would be, “It’s the uncertainty” — particularly around trade policy — that has put investors, businesses, and consumers alike back on their heels.

- Uncertainty had been building as questions around trade relations dominated in the period leading up to the Trump administration’s “Liberation Day” on April 2. Now, with the announcement of a host of tariffs levied against most of the United States’ trading partners, uncertainty has risen further.

- The tariffs announced earlier this week were much more significant than had been expected, raising serious questions about the magnitude of their impact on both growth and inflation in the near term.

- Both risks are further exacerbated by the other shoes that are starting to drop in the form of retaliatory measures by other countries. The pace of developments in the near term is likely to remain brisk, as United States’ trading partners decide how best to proceed.

- There’s been a sea change in expectations in a short period; backward-looking data like the jobs report is still valuable, but gives little to no insight into where the economy may be headed. That’s particularly true today.

Media mention:

Our experts were recently quoted on this topic in the following publication:

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.