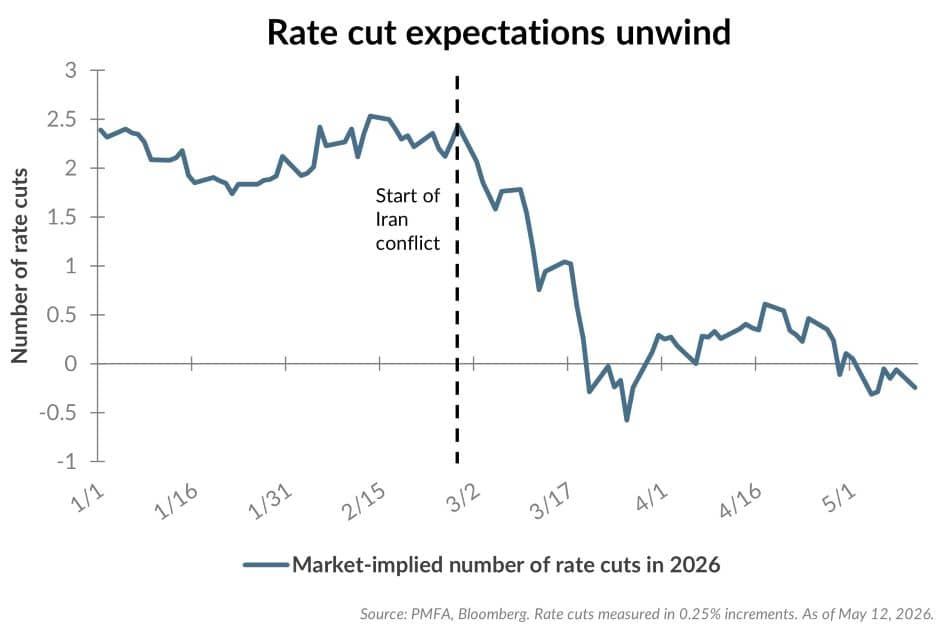

At the start of 2026, markets anticipated a continuation of the Federal Reserve’s easing cycle, with roughly two quarter-percent cuts priced into futures markets. That narrative shifted abruptly in late February as geopolitical tensions in the Middle East escalated, driving a sharp spike in crude oil prices that rippled through energy commodities, introducing renewed uncertainty into the inflation outlook. Since March, interest rate expectations have largely converged around a different baseline: an extended pause in policy — with the potential for an increase before year-end — rather than additional near-term easing.

Importantly, this shift doesn’t necessarily indicate a reassessment of the Fed’s ultimate direction but is, at a minimum, reflective of a recalibration of timing. Recent inflation data underscores the challenge. Headline CPI rose 3.8% year over year in April, with energy prices a meaningful contributor, while accelerating core inflation has moved even further above the Fed’s 2% target. At the same time, labor markets appear to be stabilizing rather than deteriorating, with unemployment holding at 4.3%, layoffs both low and stable, and payroll growth modest but positive. This combination of sticky inflation alongside a resilient labor backdrop reinforces the Fed’s need to remain patient on further easing, while raising the potential that stubbornly high inflation or rising inflation expectations could force the Fed to tighten policy.

Newly confirmed Fed Chair Kevin Warsh inherits this complex backdrop. Warsh has signaled a strong emphasis on price stability and has advocated for a disciplined approach to policy credibility. He’s also previously advocated for shrinking the Fed’s balance sheet further — a delicate balance that could create additional volatility in long-term rates. Finally, Warsh has also expressed openness to revisiting how inflation is measured, favoring trimmed metrics to better isolate underlying trends, and reducing reliance on forward guidance. Markets will be watching closely as he assumes his leadership role within the central bank for clues about his near-term focus, the potential for any meaningful shift in policy tone or execution.

All things considered, the market’s repricing in 2026 isn’t necessarily the end of a cutting cycle, but a pause extended by uncertainty. Investors will remain focused on incoming economic data, evolving inflation dynamics, and how policy direction may evolve under new Federal Reserve leadership. Each of those factors will play a meaningful role in the level of interest rates, their direction, and the potential for rate volatility across the yield curve.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.