The bottom line? Stable claims backdrop consistent with constructive labor conditions

- Boil down the report to its primary takeaway: There’s no sign of slippage for this key measure of labor market health. Positive hiring momentum has waned as the expansion has matured, but layoffs remain quite low, surprisingly stable, and consistent with a labor economy that remains on a positive footing.

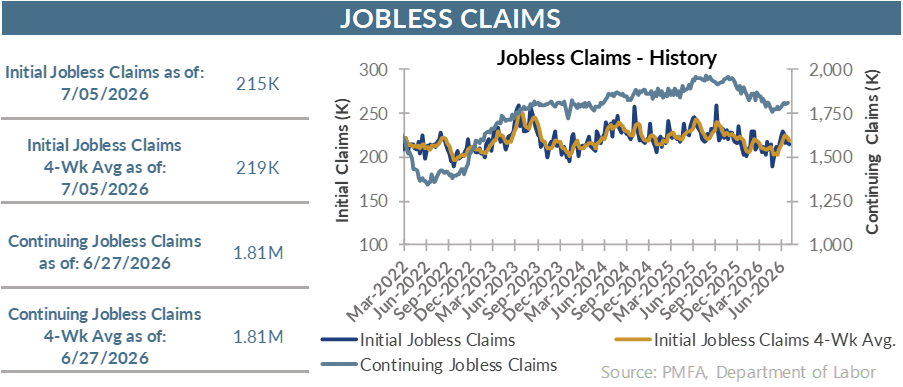

By the numbers: Steady

- Initial jobless claims were little changed last week, easing to 215,000 for the week ended July 4 from a revised 217,000. That decline also contributed to a moderation in the four-week moving average to 218,750 for the period.

- Continuing claims edged up to 1.814 million, aligned with expectations.

- Insured unemployment held firm at 1.2% and has barely budged over the past year. Recurring claims have fallen by nearly 140,000 over the past year.

What’s the story? Claims data shows a stable labor market

- The most recent weekly data drop on jobless claims checked all the boxes in a constructive manner. First-time unemployment claims are quite low — consistent with a solid labor market — and have been relatively stable in a fairly narrow range since last fall.

- Recurring claims have improved over the last year, keeping the insured unemployment rate firm at just 1.2%.

- Even as the employment situation report has delivered a more nuanced message over that period, there has been no meaningful evidence of any kind of broad-based pickup in layoffs.

- Of course, that only tells part of the story of the labor market, where hiring has been positive in recent months after a much choppier hiring environment over much of 2025.

- The recently released June jobs report delivered a much softer monthly increase in nonfarm payrolls than had been expected, while shaving previously reported estimates for April and May.

- The underlying trend for job creation is probably not as bad as the subdued — but positive — hiring data for June would have suggested. Conversely, the labor picture isn’t likely as strong as the previously reported nonfarm payroll gains in prior months indicated.

- Smooth out that monthly volatility in nonfarm payrolls and you still get to a picture of a labor economy that’s creating jobs at a pace more reasonably aligned with a maturing expansion and already low unemployment than the unsustainable hiring demand that defined a red-hot labor market just a few years ago.

- Moderation in job creation is to be expected at this stage in the cycle and not a source of alarm. It still reflects a solid growth backdrop, while also mitigating concerns that excessive tightening in labor conditions could put a renewed lift under wage growth that could exacerbate the inflation outlook.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.