The bottom line? Lower gas prices a source of relief for consumers

- It may only be at the margins, but falling gas prices should be a source of relief for consumers. That could provide more wiggle room in household budgets.

- Further, the fact that high gas prices are so easily visible makes them a crude barometer for inflation more broadly. A spike in gas prices catches the eye more quickly than for most goods; a sharp decline has a similar, positive effect. That’s readily apparent in the latest consumer sentiment data.

- Even so, consumers clearly continue to feel the burden of the price volatility and policy uncertainty that have helped to define the American economy since 2020.

- To have a reading this low during a recession wouldn’t be shocking; to have them in a period of low-unemployment and moderate growth reveals much about the disconnect between some of the key quantitative and qualitative measures of the economy today.

- At the center of the disconnect is inflation, and its corrosive effects on household spending. All feel its impact to varying degrees; it’s the common thread that remains a challenge for consumers and helps to explain the negative mood.

- A decline in prices at the pump won’t flip the script but should at least provide some relief for tight household spending budgets.

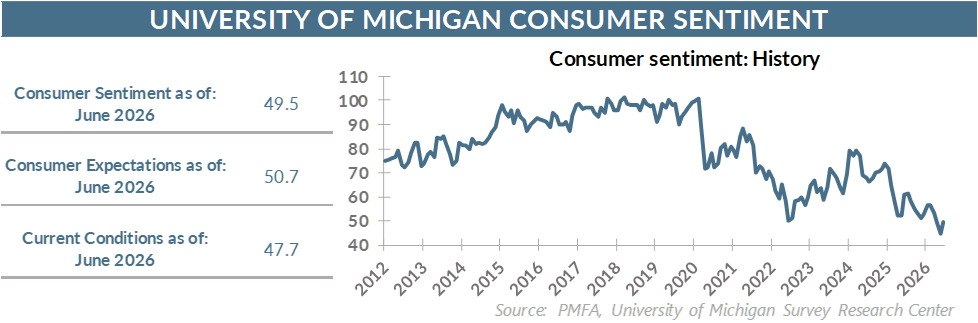

By the numbers: Sentiment gets a lift, but consumers still wary

- The University of Michigan’s Consumer Sentiment Index rose to 49.5 in June, up slightly from the historically low May reading of 44.8.

- The improvement in the index was supported by improvement in both of its underlying components, with consumers modestly more upbeat in their assessment of current conditions and increasingly optimistic about the path ahead in the coming months.

- The Index of Consumer Expectations surged to 50.7 — a 15.0% improvement in the past month. Even with that sharp bounce back, the index remains well below its level of a year ago.

- Inflation expectations for both the near- and long-term edged lower but remain elevated. It’s the problem that has become increasingly deeply rooted in recent years both in the collective consumer psyche and the real economic landscape.

Broad thoughts

- Boil it all down, and the prevailing worries for consumers are still apparent, albeit with some glimmers of hope coming into view.

- Inflation remains a major concern for most Americans, and an even greater challenge for lower- and middle-income households. At 4.6%, the one-year inflation expectation signals that households are still feeling the pinch of the significant price increases in recent years that were further exacerbated by surging gas prices earlier this year.

- Persistently higher inflation has been an unpleasant reality, but one that consumers have had to face in an economy that’s been defined in recent years by geopolitical frictions, a replumbing of global supply chains, tight labor conditions, and a material increase in tariffs.

- While not the only factor, inflation is a considerable source of the anxiety that comes through clearly in consumer surveys. Sentiment this low has typically been reserved for recessionary periods, not those characterized by solid growth and low unemployment.

- However, those two metrics alone don’t tell the whole story. The economy is growing at a decent clip, but it’s being juiced by strong business investment, largely attributable to AI-related infrastructure. The post-shutdown rebound in government spending also provided a decent lift since the beginning of the year.

- The consumer economy tells a different story: One in which spending growth has been subdued, and housing has been contracting for more than a year.

- Similarly, unemployment is low, but hiring had been choppy through much of 2025 and early this year. That tide appears to have turned in recent months, as stronger nonfarm payroll gains have provided some reassurance. Even so, many recent college graduates are struggling to find work, and youth unemployment is unusually high. It’s a labor economy that, while solid, isn’t working for everyone.

- The result is an economy that may look good on the surface but may be experienced very differently depending on which side of the job and income divide one sits.

- Layer on inflation that remains well above the Fed’s 2% target and expectations that it will remain elevated for the foreseeable future, and the subdued measures of consumer sentiment start to make sense.

- It’s the reality of the K-shaped economy, where consumption growth is increasingly driven by upper-income earners, as lower-income households are pinched by elevated inflation and interest rates, higher housing costs, and volatile gas prices.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.