With the introduction of the OBBBA and, more specifically, H.R.1, providers face unprecedented pressure driven by expanding self-pay populations caused by massive Medicaid cuts, ACA subsidy rollbacks, and new constraints on patient cost sharing. Survival in this environment requires a series of financial, operational, and strategic changes to offset the impact of an increase in uncompensated care. One immediate option is to enhance the scrutiny and accuracy of Worksheet S-10. Even a single overlooked write-off code, misclassified adjustment, or undocumented discount can result in hundreds of thousands — or millions — of dollars in lost reimbursement, while simultaneously increasing Medicare Administrative Contractor (MAC) audit exposure. Here are three actions your organization can take now.

1. Engage your finance and revenue cycle teams to revisit charity care and FAP documentation

MAC auditors don’t evaluate charity care in the abstract: They measure actual practice against the hospital’s own written policies, and any inconsistency becomes a compliance finding. Now’s the time to conduct a comprehensive review of your financial assistance policy (FAP) and bad debt processes. Core questions should guide this review should include: When was the last full update of your charity and bad debt policies? Is your self-pay discount still aligned with Amounts Generally Billed (AGB)? Has your provider roster been recently updated? Is your FAP, including the plain language summary, consistently posted at all patient-facing locations? In answering these questions, follow these key steps:

- Ensure your written FAP/charity care policy is current, consistently applied, and fully documented. MAC audits compare your practices against your own stated policies, so internal alignment is critical.

- Maintain clear eligibility criteria and ensure all determinations are fully documented in each patient file.

- Verify that all reported discounts meet FAP criteria. Exclude prompt-pay discounts, negotiated managed care discounts, or any other reductions that don’t qualify as charity care.

- Retain complete supporting documentation, including applications, screening results, approvals, denials, and financial worksheets.

Beyond the benefits to your S-10, these actions will strengthen your organization’s revenue cycle as a whole. Once the updates are complete, train staff across finance, revenue cycle, and patient access to ensure policies are implemented consistently in daily practice. When everyone understands how documentation connects to downstream reimbursement, your finance team can more accurately assess the impact on operating margins and revenue cycle outcomes.

2. Build audit-ready exhibits with general ledger tie-outs

As uncompensated care (UC) increases under the OBBBA, CMS is expected to rely more heavily on data integrity tests — not policy intent — to validate reported UC. Hospitals that can’t demonstrate clean, traceable general ledger (GL) tie-outs face disallowances regardless of actual charity care provided.

To withstand increasing S-10 audit scrutiny, your hospital must maintain clear, auditable reconciliations that connect patient-level detail, departmental summaries, and total S-10 charity care and bad debt amounts all the way to the GL and audited financial statements. A strong audit-ready process includes:

- Robust patient-level documentation. Maintain complete patient-level documentation for every line item reported on S-10, including charity care, uninsured discounts, and non-Medicare bad debt. Each encounter should clearly show: patient eligibility status, FAP determination and outcome, dates of service, amounts written off and corresponding reason codes, and insurance verification (or documentation of no coverage).

- Record retention. Retain detailed collection effort records, since MAC auditors routinely review the completeness and accuracy of all bad debt documentation.

- Alignment of discounts with FAP policies. Validate that uninsured discounts align exactly with FAP requirements. Partial-pay or zero-pay discounts should only be reported if explicitly allowed by your organization’s written FAP.

- Reconciliation of booked bad debt. Reconcile all booked bad debt amounts to both the patient accounting system and the GL. These reconciliations must demonstrate that the GL account supports the same UC amounts reported on the S-10. MAC guidance is explicit: GL tie-outs are nonnegotiable during audits. Hospitals should be fully prepared to provide exhibits establishing a clean, traceable connection between S-10 reported UC amounts and the organization’s financial statements.

The details are important from an audit perspective, but also take a step back to ensure you have reported all the UC that has already been provided — that’s where the financial opportunity lies in improving your S-10.

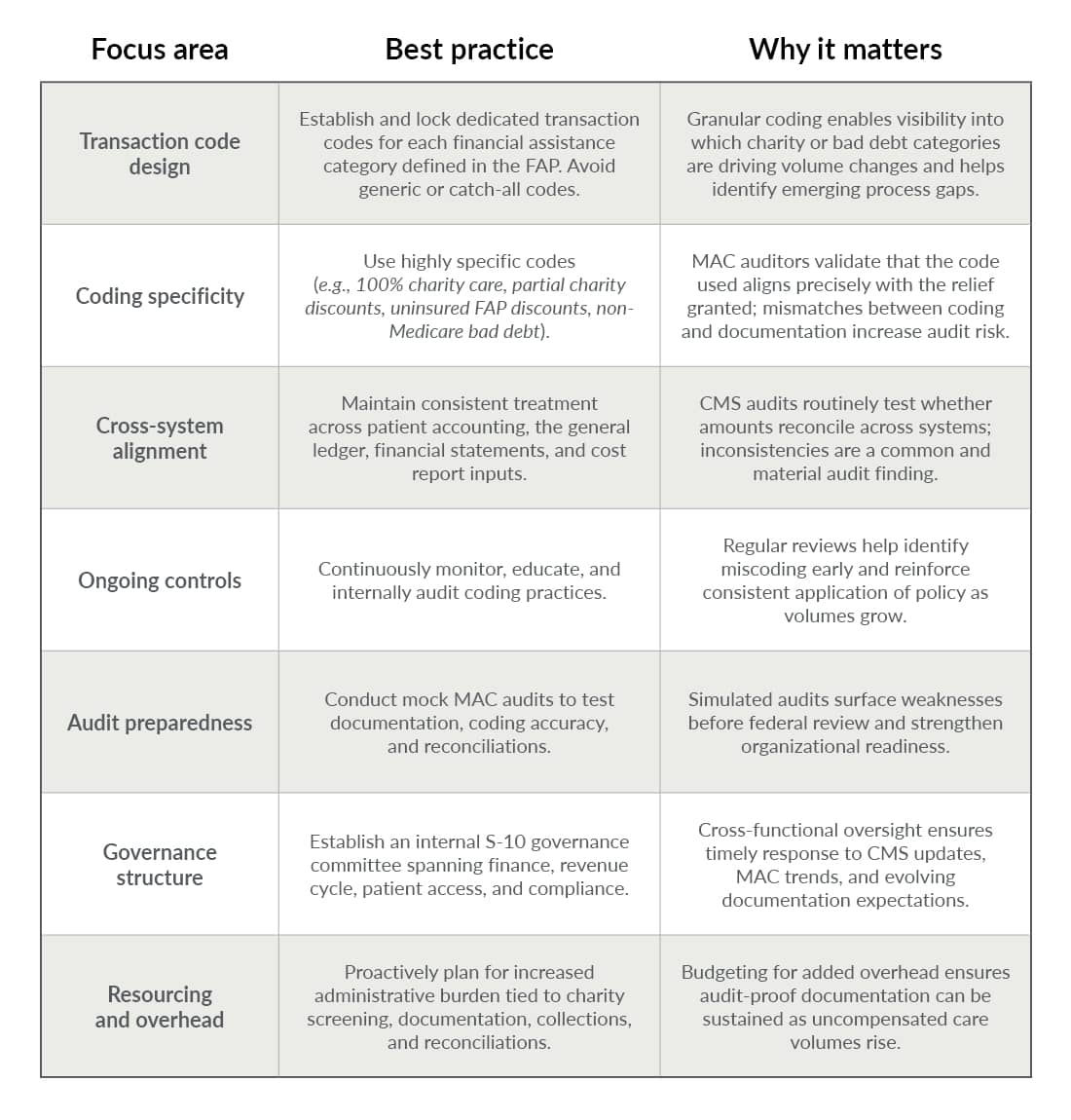

3. Lock crosswalks and transaction codes to prevent miscoding as volumes spike

Rising self-pay volume magnifies small billing weaknesses. What was immaterial at lower volumes can quickly become a material audit exposure. Standardized transaction codes — and the crosswalks that connect them to patient accounting, the GL, and cost report inputs — are essential for audit readiness and operational clarity.

Follow the best practices in the chart below.

How specialized S-10 advisors can help now

In the current environment, accuracy alone is not enough. Hospitals must also demonstrate completeness, consistency, and audit defensibility across every UC dollar reported. This is where specialized S-10 advisory support delivers measurable value.

Experienced S-10 advisors can help your hospital identify all qualifying uncompensated care across the full patient population — not just accounts tied to obvious write-off codes. Through comprehensive population scans, validation of transaction logic, and detailed policy-to-practice reviews, good advisors routinely uncover missed UC that can materially increase disproportionate share hospital-linked reimbursement.

Beyond identification, they can help your organizations prepare for heightened MAC scrutiny by building audit-ready S-10 exhibits, validating GL tie-outs, and stress-testing documentation against CMS requirements. The result is not only improved compliance, but greater confidence that every eligible UC dollar is fully captured and defensible.

Why S-10 strategy can’t wait

As CMS guidance evolves and audit activity accelerates, it’s essential to stay ahead of regulatory change, reduce rework, and protect critical reimbursement streams year over year. For organizations facing rising self-pay volume and shrinking margins, a proactive S-10 strategy is no longer optional — it’s a financial imperative. Act early to ensure your hospital is best positioned to protect revenue, reduce audit disruption, and navigate the UC surge with confidence.