First, the bottom line: This is, at worst, a very solid report

- There was a lot more to like in the May jobs report than not. Job creation was much stronger than anticipated, extending an encouragingly solid pace in recent months.

- If anything, a string of three consecutive months of solid job gains should raise the question of whether the “no hire, no fire” characterization of labor conditions that persisted over much of the past year is still accurate.

- Jobless claims are still very low, validating the “no fire” aspect of the current labor economy. It’s harder to make the case that it’s still a “no hire” environment with the three-month average payroll gain at 188,000. That’s a far cry from the choppy, but low, job creation environment that helped to define the economy last year.

- For a Fed that’s undergoing a leadership transition, the report further diminishes the case that the economy needs any further accommodation via lower policy rates. There appears to be no pressing need for the Fed to reverse course in the near term, but a further shift toward a hiking bias while holding rates steady for the time being wouldn’t be surprising.

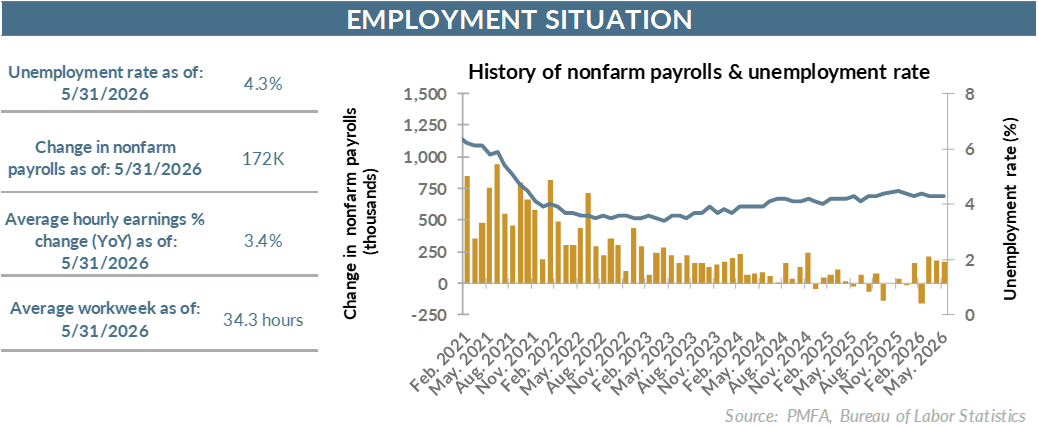

By the numbers: Strong job gains set the tone for the May report

- Nonfarm payrolls surprised to the upside with a 172,000 increase in May, nearly doubling recent forecast gains for the month.

- On the strength of those job gains, the unemployment rate held firm at 4.3% for the third consecutive month.

- Average hourly earnings rose by 0.3% in May and have risen by 3.4% over the past year.

Broad thoughts: One more data point supporting a bias toward higher rates, but an imminent move isn’t likely

- The new Federal Open Market Committee chair, Kevin Warsh, was selected in part for his vocal support for reducing the Fed’s balance sheet and a bias toward reducing interest rates. On the latter goal, today’s release of the May jobs report won’t help.

- As Fed policymakers weigh the balance of data between the case for a rate cut and one for a rate increase, the surprisingly strong May jobs report lands unambiguously on the growing stack of arguments against further easing. But whether that will ultimately translate into a rate increase in the near term remains to be seen.

- The so-called insurance cuts delivered by the Powell Fed last fall came at a time in which job creation was see-sawing month to month. Positive monthly gains were generally soft, punctuated with offsetting monthly losses, which suggested that over a multi-month time horizon, hiring was grinding to a near standstill.

- There’s growing evidence that the labor economy has broken out of its period of instability and that employers are leaning back into a more front-footed stance on hiring. Solidifying labor conditions makes the case for a rate cut more difficult, particularly against the backdrop of resurgent inflation.

- Fed funds futures have already pivoted in recent months, stepping back from earlier expectations for further Fed rate cuts, instead leaning toward incremental tightening by the end of the year.

- What we don’t know is how the Warsh-led Fed will view the current inflation surge given the nature of its primary catalyst, or how much that will influence their perceived need to take action. The global supply shock and resulting spike in crude oil prices isn’t going to be solved with tighter Fed policy. If anything, higher interest rates would exacerbate the strain felt by a large swathe of American consumers.

- A reopening of the Strait of Hormuz and resumption of global oil flow would do much more to address the primary cause and help alleviate near-term inflation concerns than would a higher Fed policy rate.

- Even so, if the rate cuts of last fall were delivered to provide support and reassurance to a labor economy that increasingly appears to be finding its footing as tariff-related uncertainty fades, there’s a growing case to be made that the need to maintain more accommodative policy has diminished.

- Every month of solid job creation reduces the potential that any surprisingly positive data point is an anomaly, but instead a signal that hiring has more sustainably regathered momentum.

- The combination of solid hiring, limited layoffs, and low unemployment are indicative of a labor market that may not be at full employment, but it’s in a much better position than was feared when the Fed started cutting rates last fall.

- That doesn’t mean that the Fed will feel any need to tighten in the near term. Wage gains remain in a constructive range that shouldn’t contribute negatively to inflation concerns. That should afford the Fed more flexibility to remain on hold, potentially giving more time for oil prices to stabilize, if not recede.

- For now, the data should broadly give Fed Chair Warsh time to settle into his new role without an imminent need to disrupt current policy. That likely translates to keeping rates on hold for an extended period, but with a bias toward modest tightening rather than further cuts, so long as the hiring environment sustains its newfound momentum.

Past performance does not guarantee future results. All investments include risk and have the potential for loss as well as gain.

Data sources for peer group comparisons, returns, and standard statistical data are provided by the sources referenced and are based on data obtained from recognized statistical services or other sources believed to be reliable. However, some or all of the information has not been verified prior to the analysis, and we do not make any representations as to its accuracy or completeness. Any analysis nonfactual in nature constitutes only current opinions, which are subject to change. Benchmarks or indices are included for information purposes only to reflect the current market environment; no index is a directly tradable investment. There may be instances when consultant opinions regarding any fundamental or quantitative analysis may not agree.

Plante Moran Financial Advisors (PMFA) publishes this update to convey general information about market conditions and not for the purpose of providing investment advice. Investment in any of the companies or sectors mentioned herein may not be appropriate for you. You should consult a representative from PMFA for investment advice regarding your own situation.

.jpg?la=en&h=307&mw=480&w=480&hash=6A627DBF766882E4EE1BC9926E34CB08)