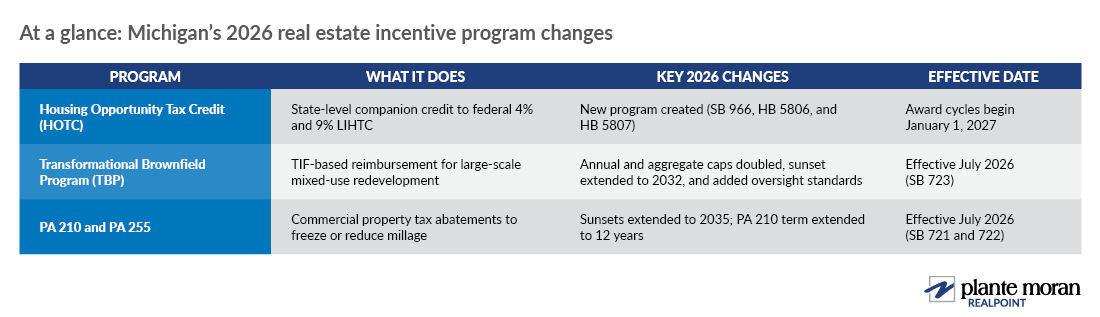

Michigan lawmakers closed out a marathon session before the holiday weekend to pass Michigan’s next budget — and additionally passed significant measures to create, expand, or extend real estate economic development programs within the state.

This article provides an overview of these legislative changes and how they will benefit investments in affordable housing, mixed-use development, and commercial redevelopment in the State of Michigan. Key takeaways are summarized here, but read on for more detailed information:

- New Housing Opportunity Tax Credit (HOTC): A new state companion credit to federal 4% and 9% Low-Income Housing Tax Credits (LIHTCs) could generate roughly $160 million in tax credit equity annually, supporting an estimated 4,000 new affordable housing units per year beginning with the 2027 award cycle.

- Transformational Brownfield Program (TBP) expanded: The annual and aggregate caps on State Tax Capture Revenues (STCRs) double to $160 million per year and $3.2 billion total, unlocking stalled projects such as the Renaissance Center redevelopment in Detroit and redevelopment projects on Grand Rapids’ riverfront.

- Commercial property tax abatement programs extended: Both PA 210 and PA 255 programs receive a 10-year sunset extension (to Dec. 31, 2035), preserving tools that were otherwise set to expire at the end of 2025.

- Extends program sunset to December 31, 2032.

- Increases annual program cap from $80 million to $160 million for STCRs and includes a specific provision stating that the $80 million increase must be wholly attributable to “new” TBPs.

- Increases total program cap from $1.6 billion to $3.2 billion for STCRs.

- Provides greater flexibility in the definition of “base year” for the purpose of establishing incremental values within a TBP work plan.

- Removes the complex plan distribution so that plans must now be approved and distributed equally “as practicable.”

- Adds a “withholding disqualified employees” and “… entities” concept, effectively limiting withholding tax capture to “new jobs” only.

- Requires new plans to use the “safe harbor method” for income tax capture and withholding tax capture.

- Requires an “affordable component” within any TBP approved that contains residential housing.

- Requires a minimum of 20% of the units to be affordable within a project for it to be eligible for 100% income tax capture (versus 50% without any affordable component).

- Requires a reimbursement agreement to include “project milestones” (i.e. construction start, completion dates, etc.) that must be met to capture taxes or continue to capture taxes.

- Expressly limits CPTCRs to five years after the plan’s approval.

- Adds a third-party underwriting and fiscal benefit analysis to the state for TBPs proposing to use either more than $10 million in annual STCRs or more than $100 million in actual capital investment with the safe harbor method for STCRs.

- Significantly increases public reporting requirements for the Michigan Strategic Fund and MEDC regarding TBP project status, tax capture received, and projected future tax capture revenues through the addition of Section 16 to Act 381.

- Enacts stricter procedures if a minimum investment threshold is not met.

- Implements a $200 million program limit for approved CPTCRs and the Construction Period SUTE, and specifically excludes previously approved Construction Period SUTEs.

- Implements a $300 million limit for any plan in approved CPTCRs, Construction Period SUTE, and STCRs.

Housing Opportunity Tax Credit

The Michigan State Housing Development Authority (MSHDA) was created under Public Act (PA) 346 of 1966 and provides financial and technical assistance to support affordable housing, homeownership, and community development across the state. MSHDA administers the state’s allocation of key financing resources to support the creation or preservation of affordable housing, including 4% and 9% LIHTCs, tax-exempt bonds or loans, and other state and federal gap financing resources (e.g., HOME funds, Housing Trust Funds, etc.).

Affordable housing projects are fundamentally resource constrained. MSHDA’s Round 19 Gap Funding Program made $40 million in gap financing resources available and received $225 million in requests from the development community, highlighting how significantly these programs are underfunded relative to the demand.

New tax credit program created

In May 2026, the State Senate introduced Senate Bill 966, along with two other tie-barred bills (House Bill 5806 and House Bill 5807). The centerpiece: the creation of a state-level Housing Opportunity Tax Credit (HOTC) program that pairs with the federal LIHTC programs.

During Senate floor debate, Senator Jeff Irwin (D-Ann Arbor), the bill’s sponsor, cited roughly 200,000 low-income Michigan households currently without access to affordable housing. Michigan's broader housing production goal (raised from 75,000 to 115,000 new or rehabilitated units under the Whitmer Administration after the original goal was met early) stood at approximately 87,000 units as of early 2026.

This new program provides a crucial additional resource for affordable housing development within the state and follows in the footsteps of dozens of other states that have successfully implemented state-level companion credits for federal tax credit programs.

HOTC program structure

The HOTC program will be administered by MSHDA, with applications being accepted in conjunction with MSHDA’s existing LIHTC programs. Award cycles will begin on January 1, 2027. The state has approved a base annual credit amount of $42 million, which will be increased annually by the Consumer Price Index. Any unused or recaptured credits may be rolled forward into future award cycles.

HOTC’s credit considerations

The credit period is for six calendar years, beginning when the building is placed in service (this is shorter than the federal 10-year credit period). The annual credit awarded to a project cannot exceed the lesser of either the amount necessary for financial feasibility or the adjusted annual federal credit amount (defined as one-sixth of the aggregate federal credit allocated to the project). The HOTC program is structured to effectively double the gross credit value of the 4% LIHTC program.

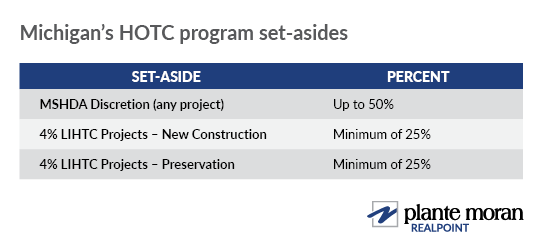

HOTC administration & set-asides

The HOTC application windows are planned for Q1 and Q3 each year, mirroring how the 9% LIHTC program is administered. At least 45% of the award cycle credit cap is reserved for 4% LIHTC qualifying projects, leaving flexibility for MSHDA to pair the HOTC with 9% LIHTC to stretch those limited resources even further. Stated set-asides within the approved legislation are outlined in the table below.

Additionally, to the extent that enough applications are received for relevant projects, at least 30% of the amounts set aside above will be allocated to qualified projects located in rural areas, which are defined as cities, villages, or townships with a population of 35,000 or fewer. Lastly, MSHDA must give preference to projects using building components manufactured in Michigan in a process that is still to be determined by MSHDA but will consider the impact on total development costs.

HOTC’s economic value

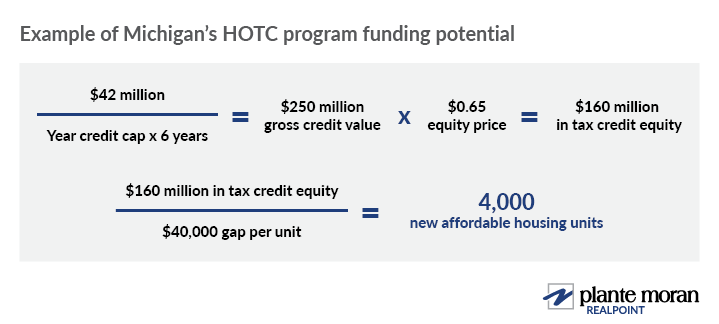

The HOTC program has the potential to create thousands more affordable housing units per year. Take, for example, the Round 19 Gap Funding Program. About $225 million of gap financing was requested for more than 5,500 potential affordable housing units, resulting in a “gap per unit” of roughly $40,000. The present equity value of the $42 million credit over six years is potentially an additional $160 million in annual financing value to close gaps in financing, which, at $40,000 per unit, would result in an additional 4,000 affordable units being funded.

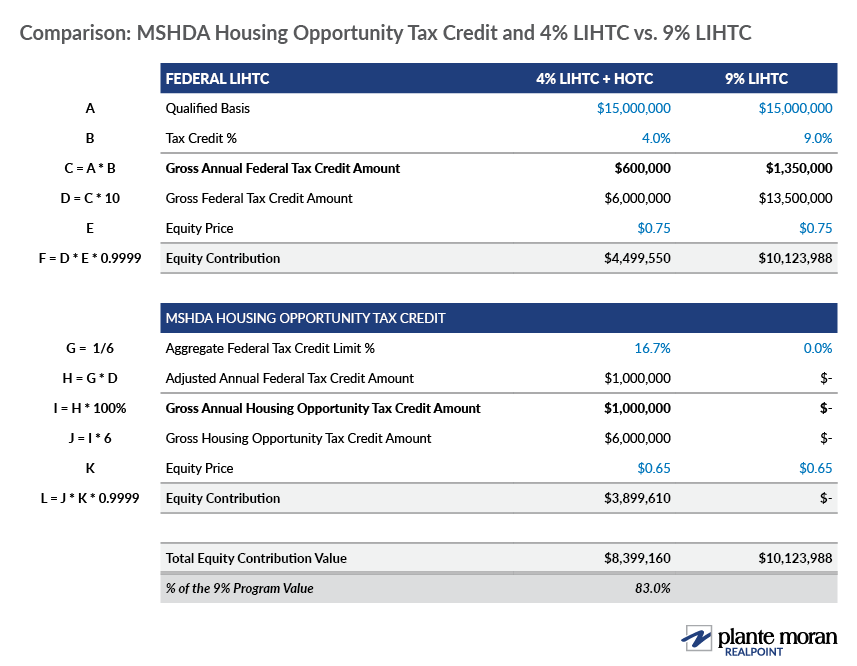

Pairing the HOTC program with the 4% LIHTC program will be highly effective at minimizing gaps in affordable housing pro formas. The table below illustrates how the two resources combined compare to a traditional 9% LIHTC in terms of tax credit equity contribution value. This example is for illustrative purposes only; as noted above, the HOTC may be paired with the 9% LIHTC program.

Developer considerations

This program can enable developers to reevaluate deals that were previously infeasible due to large financial gaps. The rural, new construction, and preservation set-asides mean project type and location will affect competitiveness for a share of the annual $42 million HOTC pool. This will need to factor into developers’ site selection and deal sourcing now, ahead of the first 2027 award cycle. Given HOTC’s shorter credit period (six years versus 10 years for federal), underwriting pay-in schedules and equity pricing will vary from federal LIHTC programs.

Transformational Brownfield Program

The State of Michigan’s Brownfield Redevelopment Financing Act (Act 381 of 1996) enables real estate developers to use the new property taxes generated from their investments (known as tax increment financing or TIF) to reimburse themselves for qualifying costs related to cleaning brownfield (i.e., environmentally contaminated) sites.

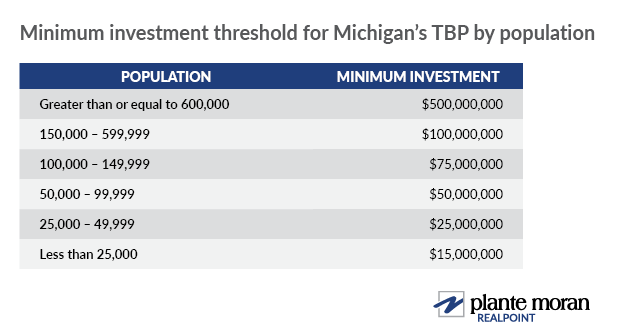

In 2017, Act 381 was amended to include the Transformational Brownfield Program (TBP). TBP supports large-scale, mixed-use developments on sites that qualify under the traditional Brownfield TIF program and have a transformational impact on a city’s population, commercial activity, or employment. Transformational plans require a minimum capital investment ranging from $15 million in small communities to $500 million in large municipalities.

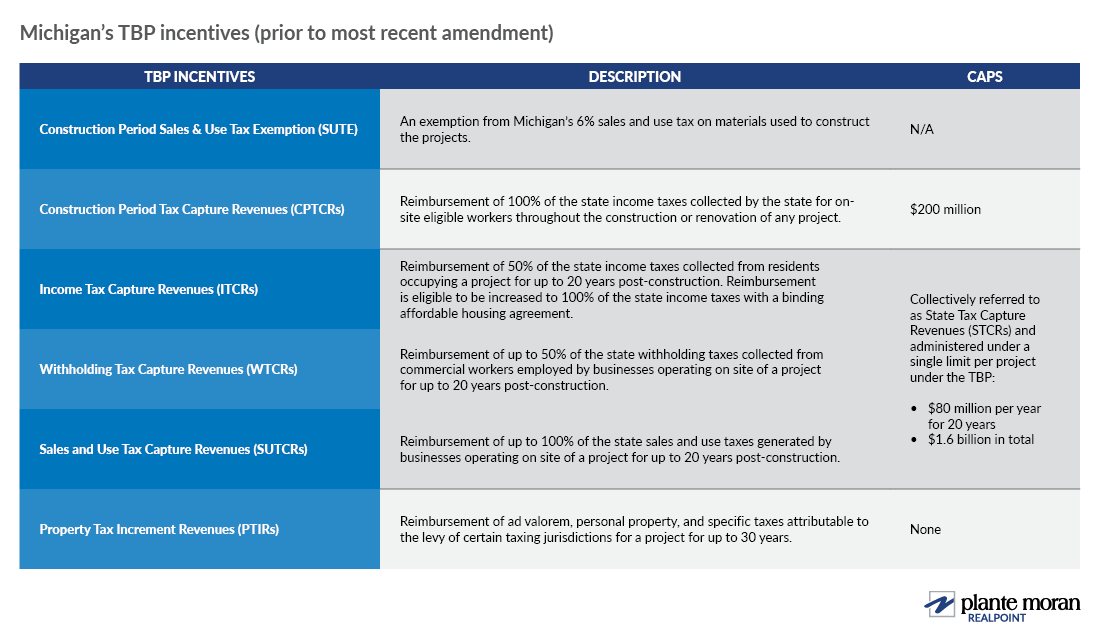

Qualifying projects and development plans are eligible to receive tax capture revenues and tax exemptions as forms of reimbursement for eligible activities (defined as vertical construction costs under the TBP) as described in the table below.

TBP program changes

The TBP resources are available on a first-come, first-served basis for qualifying projects, as reviewed by the Michigan Economic Development Corporation (MEDC). Since 2025, the program has been unable to accept new applications requesting the STCRs as the limits have been met, leaving several major projects throughout the state in limbo.

In December 2025, Senate Bill 723 was introduced, focusing on extending and expanding the TBP, preserving its core state tax capture incentives while adding greater standards, oversight, and flexibility provisions.

TBP’s program expansion and increased flexibility provisions:

TBP’s greater oversight and standards provisions:

TBP’s economic value

TBP differs from traditional brownfield TIF programs by adding STCRs as a form of reimbursement to incentivize development.

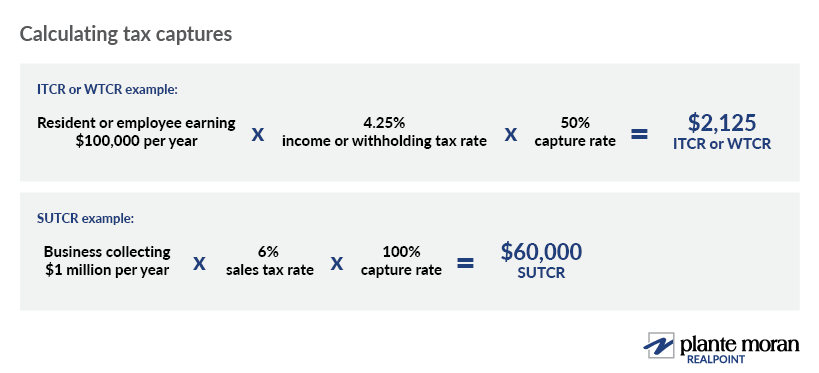

Take, for example, a resident or employee earning $100,000 per year. Within TBP, the developer is eligible to capture 50% of the 4.25% state income or withholding taxes paid by that resident or employee, meaning the developer will receive $2,125 per year in ITCR or WTCR for every resident or employee that occupies a TBP project after completion. Similarly, developers are eligible to capture 100% of the 6% state sales tax collected by businesses located at TBP properties. If a business collects $1 million in taxable sales per year, the developer will be reimbursed $60,000 per year in SUTCR for that business.

To date, TBP has supported nearly $8 billion in total planned investment, more than 8,000 residential units, more than 18,000 full-time jobs, and millions of square feet of commercial and residential development. With the aggregate and annual caps of STCRs doubling and the sunset extended to 2032, the program is well positioned to continue to be a catalyst of transformative mixed-use developments within Michigan.

Developer considerations

Resources for the program are anticipated to be competitive, with only 14 plans approved under the previous cap, and several large projects already in the pipeline. The added requirement for third-party underwriting and fiscal analysis will increase application costs for plans of investment greater than $100 million. The added affordability requirement for any plan including residential will also change traditional project economics, though the ability to capture 100% income tax capture for plans exceeding 20% of units as affordable will be meaningful in any cost/benefit analysis.

Commercial Property Tax Abatements

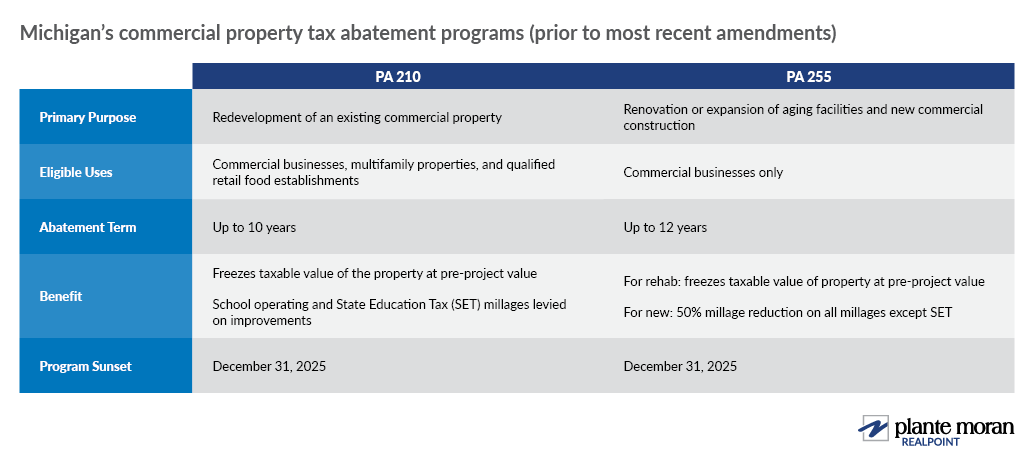

The Commercial Rehabilitation Act 210 of 2005 (PA 210) and the Commercial Redevelopment Act 255 of 1987 (PA 255) are two keystone property tax abatement tools designed to encourage private investment in commercial real estate. Both programs freeze property taxes on commercial property and reduce the applicable millages applied to improvements.

Changes to commercial property tax abatement programs

In December 2025, Senate Bills 721 and 722 were introduced to extend both programs’ sunset to December 31, 2035, and extend the maximum abatement term for PA 210 to 12 years. Both bills were adopted and approved on July 3, 2026.

Commercial property tax abatement programs’ economic value

These two commercial property tax abatement programs are tried-and-true tools for encouraging commercial development throughout the state. Their extension will continue to enable developers to navigate Michigan’s high property tax environment and, further, helps enable Michigan to remain competitive with neighboring Midwest states with lower or comparable property rates (such as Indiana, Ohio, and Wisconsin). Michigan ranks 14th highest in the United States for effective property tax rates, and the City of Detroit distinctly has the highest effective property tax rate among large cities in the country.

Developer considerations

Developers should confirm PA 210 versus PA 255 eligibility early and ensure millages rates are being appropriately applied in new construction and rehabilitation scenarios. Both abatements are limited in term to 12 years; developers should be appropriately modeling abatement benefits while managing burn-off risk and associated impacts to financing and exit values.

Takeaways for developers

For developers, these legislative changes represent more than incremental program updates. They create new opportunities to improve project feasibility, close financing gaps, and advance projects that may otherwise be difficult to execute in today’s cost and capital environment. Understanding how the HOTC, TBP, and commercial property tax abatements can work individually or together will be critical as projects move from concept to execution.

Plante Moran Realpoint is a full-service real estate advisory firm with experience supporting public and private clients as they evaluate, structure, and pursue economic development incentives. Contact our team with questions about how these changes may affect your next Michigan development or redevelopment project.